The U.S. labor market slowdown has officially started. Ignore all the political commentators because the August’s jobs report was a reality check, and Q4 is shaping up to be tough. Let’s break it down and ask the hard questions policymakers, executives, and workers need to face.

Benchmark key workforce metrics in your company – Access database

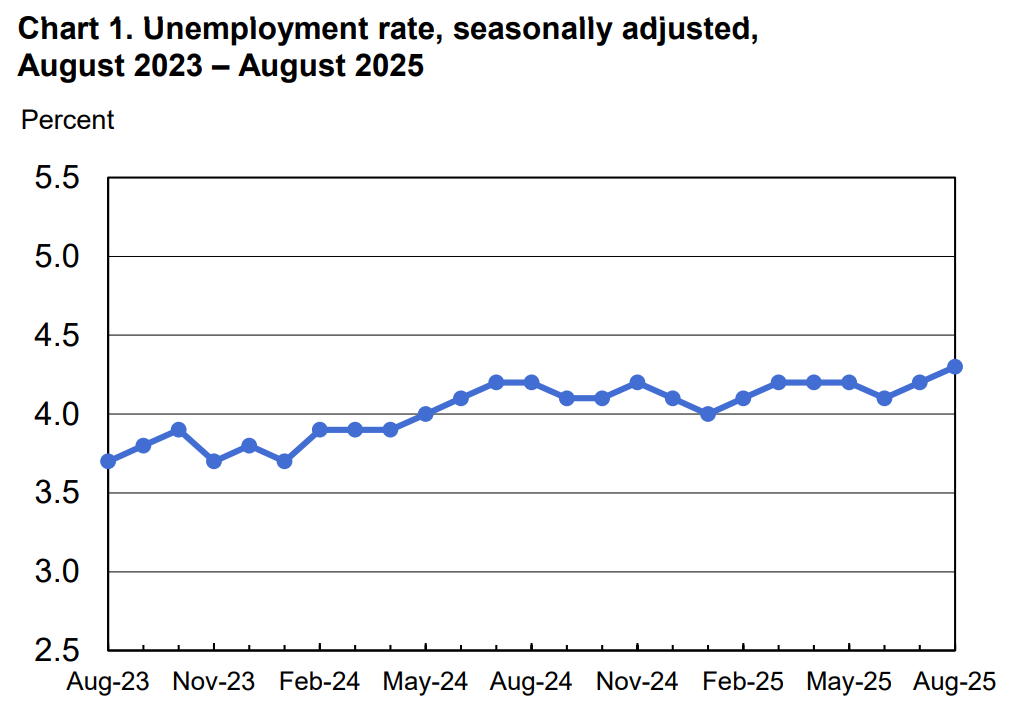

In August, the Bureau of Labor Statistics (BLS) reported that payrolls grew by just 22,000 jobs, while the unemployment rate rose to 4.3%, the highest level since 2021. To make matters worse, June’s job gains were revised into an outright loss, officially ending a 52-month streak of expansion. Employers aren’t just slowing down hiring - They’re actively retrenching, and that’s a major shift from the narrative of “resilient” labor markets we’ve been hearing all year.

This is the moment when policymakers and economists must confront reality: if job creation has essentially stalled, can we really still talk about a soft landing? Or have we already veered into a hard slowdown that risks tipping into something deeper?

The overall numbers hide sharp differences across industries. Healthcare and social assistance are still expanding, adding around 31,000 jobs in August (BLS), but the pace is slower, and job postings are already slipping. Retail and manufacturing, two pillars of middle-class employment, are flashing red. Retail job postings have dropped by double digits, and manufacturing payrolls are shrinking month after month. These are industries that reflect the health of consumer demand and industrial output. When they drop, the whole economy feels it, and quickly.

Federal and state employment are also under pressure. Mass layoffs at the federal level, including large-scale agency cutbacks, are further weakening public-sector job stability. At the same time, digital-first industries are bucking the trend. Software, internet services, and remote-enabled roles continue to grow, with some subcategories showing double-digit posting increases. The story is clear: U.S. workers with digital skills remain in demand, while those tied to traditional industries face an increasingly precarious landscape.

Beyond the headline payroll numbers, underlying indicators also look troubling. Looking back a bit further in this quarter, job openings fell to 7.18 million in July, one of the lowest readings since the pandemic. The hiring rate slipped to 3.3%, signalling that companies are pulling back significantly. For job seekers, the situation is even harsher: 1.9 million Americans have been unemployed for 27 weeks or longer, making up over a quarter of the jobless population (BLS).

On the supply side, demographic and policy factors are squeezing the labor market further. OECD reported that immigration has slowed dramatically, and with an aging U.S. workforce, the pool of available labor is shrinking. Analysts at Reuters have suggested that monthly payroll growth could slow to fewer than 10,000 jobs under these constraints.

If demand is falling because employers are cutting back and supply is drying up because of demographics and immigration policy, is the U.S. labor market approaching a structural crisis rather than a cyclical slowdown? We hope not, but it is increasingly looking that way.

Be the most informed leader in the room - Get benchmarks

Markets are convinced the Federal Reserve will step in with rate cuts. Following the August jobs report, Kiplinger reported that expectations surged for a 25 basis point cut in September, with investors betting on additional cuts by the end of the year. Some policymakers still argue the economy has enough momentum to accelerate in Q4. But this optimism seems increasingly detached from labor market data.

Let’s be blunt: if the Fed has to cut rates while unemployment is rising, long-term unemployment is climbing, and job creation is sputtering, isn’t that essentially an admission that growth is already on the brink? Rate cuts might provide temporary relief, but they can’t generate demographic growth or reverse structural labor shortages.

All of this negative noise has an impact on the business sector. The Wall Street Journal stated that nearly 20% of U.S. firms say they plan to slow hiring in the second half of 2025, with health care, staffing, and tech leading the pullback. This shows that companies are becoming more cautious, holding off on new projects, and waiting to see what happens next in the economy. The risk is that if too many firms cut back at the same time, it could make the slowdown worse by reducing jobs, spending, and overall confidence.

The outlook isn’t rosy. Ernst & Young projects job growth averaging only 25,000 per month through the end of 2025, with unemployment creeping up to 4.8% by early 2026. Analysts at the Washington Post warn that recession odds are hovering around 50%. Yes, there’s potential upside from AI-driven investment or new industrial policy, but the risks of missteps remain far greater as it currently stands.

For business leaders, the message is clear: Prepare for more economic uncertainty and a likely continued softening of the jobs market, reallocate capital toward digital-first growth sectors if possible, and stress-test your hiring and investment plans against multiple scenarios.

For workers, the picture is gloomy. The average job search now drags on for 24 weeks, nearly half a year without steady income (WSJ). If you’re not upskilling in AI, you’re probably falling behind relative to the rest of the workforce. As the old saying goes "you never stop learning in life", and now is the time to learn about (and experiment with) AI as much as you can.

For policymakers, immigration caps and an aging workforce are squeezing labor supply. Rate cuts are unlikely to solve this alone. So, will leaders acknowledge the reality of structural constraints, or will they keep papering over cracks with monetary easing? Only time will tell.

The U.S. labor market has reached an inflection point. The slowdown isn’t “coming” - It’s already here. Q4 2025 will test whether America can adapt to a digital-first economy while grappling with demographic decline and corporate caution. If we keep pretending this is just a temporary blip, the slowdown may harden into something far worse.

At CompanySights, the tough question that we’re asking our clients is simple: Are you prepared for a job market that looks nothing like the one we’ve known for the past decade?

Explore benchmarking data to evaluate your workforce

.svg)

Download a copy of our latest all industry report with data to benchmark the Finance, HR, IT and Marketing functions.

Insights are just around the corner.

.svg)

.svg)